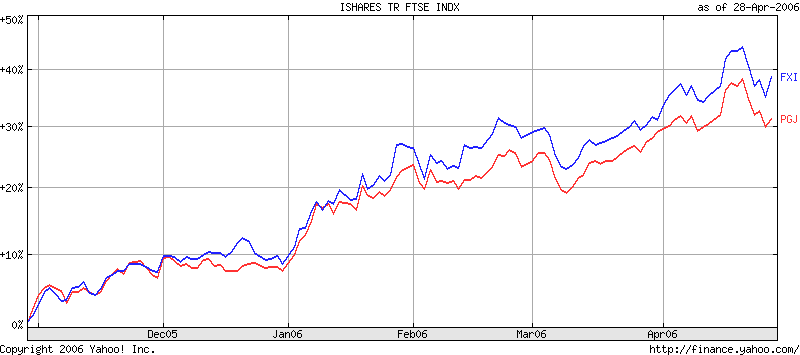

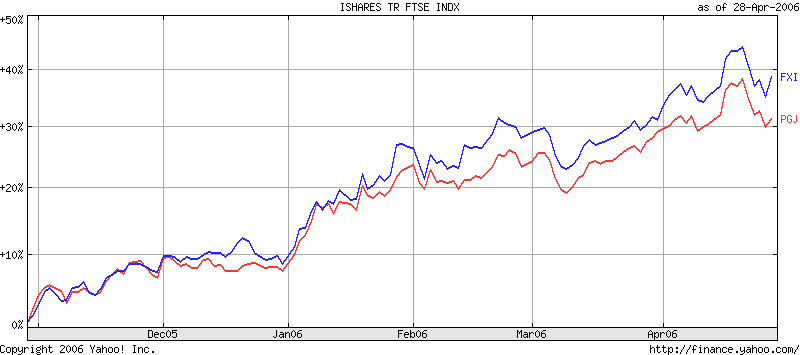

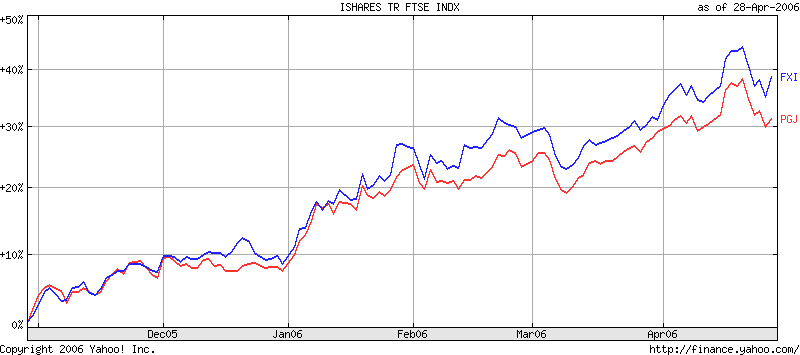

In the previous articles we discussed about investing in

China and other

emerging markets. We also discussed investing in

India and the

mutual fund options for investing in India. In the prior article on investing in China, we looked at the companies listed in NYSE. One of them is Petro China (PTR). Warren Buffet has quintipled his investment in Petro China in the course of last several years. In this segment we will look at Chinese companies listed in NASDAQ. In the upcoming segments we will go deeper into some of the companies and mutual funds investing in the middle kingdom.

(ASIA)AsiaInfo Holdings, Inc.The best introduction for this company is from the company's website.

AsiaInfo Holdings, Inc. (Nasdaq: ASIA) is a leading provider of high quality telecom software solutions and security products and services in China. The company provides total customer solutions to some of China's largest companies, and helps its customers to increase their business value in fast-growing and evolving markets. AsiaInfo's products and services cover:

(1) telecom network infrastructure and application services, encompassing messaging, broadband and wireless; customer relationship management (CRM) and billing solutions; decision support systems; business intelligence (BI); and human resource management (HRM).

(2) Security products and services, including firewall, VPN, IDN and security management services.

Organized as a Delaware corporation, AsiaInfo has constructed national backbones and provincial access networks for all of China's major national telecom carriers since 1995, including China Telecom, China Mobile, China Unicom and China Netcom. Since 2000, the company has successfully shifted its focus from Internet infrastructure construction to the provision of a full suite of telecom software solutions.

Following its acquisition of Lenovo's non telecom IT businesses in 2004, AsiaInfo is now one of the top providers of security products and services in China.The company has a market cap of 217 million and EPS of -0.83.

(CTRP)Ctrip.com International Ltd.This company may be called the Chinese Expedia. As anyone familiar with the expedia story, one can ride the horse for a while before getting off. This company should be no different, but has some ride left in it. The company currently has a P/E of 50 and a market cap of 1.4 billion. Compare this with expedia - which carries a market cap of 6.65 billion and a P/E of 30.

(LTON)Linktone Ltd.Linktone carries a P/E of 17 with a market cap of 194 million. As noted in Yahoo! Finance, Linktone, Ltd. provides wireless media, entertainment, and communication services to mobile phone users in the People’s Republic of China. It engages in the development, aggregation, marketing, and distribution of consumer wireless content and applications for access by mobile phone users. The company offers entertainment-oriented wireless value-added services over the second generation (2G) and the 2.5G mobile telecommunications networks. Linktone’s 2G short messaging services-based services include ringtones, icons and screen savers, interactive SMS messaging in certain television programs, adventure, action, trivia and fortune-telling games, lunar and western horoscopes, POP messaging, jokes, fan clubs, event-driven or entertainment news updates, and a virtual mobile amusement park called WonderWorld.

(NTES)Netease.com, Inc.From NetEase.com website,

NetEase.com, Inc. is a leading China-based Internet technology company that pioneered the development of applications, services and other technologies for the Internet in China. Our online communities and personalized premium services have established a large and stable user base for the NetEase websites which are operated by our affiliate. The NetEase websites had more than 786 million average daily page views for the month of December 2005, making us one of the most popular destinations in China and on the World Wide Web. In particular, NetEase provides online game services to Internet users through the licensing or in-house development of massively multi-player online role-playing games, including Westward Journey Online II, Fantasy Westward Journey and Fly for Fun. NetEase also offers online advertising on its websites which enables advertisers to reach our substantial user base. In addition, NetEase has paid listings on its search engine and web directory and classified ads services, as well as an online mall, which provides opportunities for e-commerce and traditional businesses to establish their own storefront on the Internet. NetEase also offers wireless value-added services such as news and information content, matchmaking services, music and photos from the Web which are sent over SMS, MMS, WAP, IVR and Color Ring-back Tone technologies. Other community services which the NetEase websites offer include instant messaging, online personal ads, matchmaking, alumni clubs, personal home pages and community forums. NetEase is also the largest provider of free e-mail services in China. Furthermore, the NetEase websites provide more than 17 channels of content. NetEase aggregates news content on world events, sports, science and technology, and financial markets, as well as entertainment content such as cartoons, games, astrology and jokes, from over one hundred international and domestic content providers. The company has been consistently growing profts since inception ( 1997 ) and a market cap of 3 Billion and a P/E of 29.

(SNDA)Shanda Interactive Entertainment

SNDA engages in the development and operation of online games in China. It offers a portfolio of online games, which users play over the Internet. The company’s content offerings primarily consist of online games, including massively multiplayer online role playing games (MMORPGs) and casual games. MMORPGs are action-adventure based, and draw upon martial arts and combat themes. Casual games are session-based, which can be played to a conclusion within a short period of time. The company has a market cap of 936 million and a P/E of 47. The company has earnings of 0.28/share.

(XING) Qiao Xing Universal Telephone

From Yahoo! site,

Qiao Xing Universal Telephone, Inc. engages in the manufacture and distribution of telecommunications products. Its product portfolio includes telecommunications terminals and related products, including fixed wireless phones and mobile phones; and consumer electronics, such as MP3 players, cash registers, and set-top-box products. The company also designs fixed line telephones and GSM mobile phones. Qiao Xing Universal distributes its products through independent regional distributors, and after-sales service centers, including wholesale agencies in China. As of December 31, 2004, the company distributed its products through 40 regional distributors to approximately 5,000 retail outlets in China. It has strategic partnership relationships with China Telecom, China Netcom, China Railcom, China Mobile, and China Unicom. The company was founded by Rui Lin Wu in 1992 and is based in Huizhou City, People’s Republic of China.

Xing has a market cap of 149 million and a P/E of 52. The company earns 0.17 cents/share.

(SINA)Sina.com

From Yahoo! finance, SINA Corporation operates as an online media company and information services provider in China. The company provides an array of services to its users, including region-focused online portals, mobile value-added services, search and directory, interest-based and community-building channels, free and premium email, audio and video streaming, online games, virtual ISP, classified listings, electronic-commerce, and enterprise electronic solutions. Its advertising offerings include banner, button, and text-link advertisements that appear on pages within the SINA network. SINA has a market cap of 1.41B and a P/E of 36. The company earns 75 cents/share.

(SOHU)Sohu.com, Inc.

Sohu primarily offers content, brand advertising, sponsored search, wireless, e-commerce, and online gaming services through its Internet portal sites. The company has a market cap of 941 million and a P/E of 33. The earnings per share is 0.77.

(TOMO)Tom Online Inc

TOM Online’s primary business activities include wireless Internet services and online advertising. The company’s wireless Internet services comprise wireless Internet data services and wireless Internet voice services. In some sense TOMO and BIDU are competitors. Tomo has a market cap of 1.46 Billion and a P/E of 32.31. The company has earnings of 0.85/share.

(BIDU) Baidu.com, Inc.

Baidu offers search services in Chinese language. The company is profitable. The EPS for the company is 0.19 and a P/E of 310. The company has a market cap of 1.89 Billion overall.

(CMED) China Medical Technologies Inc.

The company's website provides a good snapshot of the company.

China Medical Technologies Inc. is a high-Tech enterprise of trading at Nasdaq with the ticker-CMED. We currently conduct our operation principally through our wholly-owned subsidiary Beijing Yuande Bio-Medical Engineering Co.Ltd. in China. Yuande was established in 1999 and its headquarters and manufacturing facilities are located in Bejing Economical and Technological Development Area. The company was awarded ISO9001 certification in 2001. Cooperated with researchers from Peking University, we have developed High Intensity Focused Ultrasound (HIFU) tumor therapy system through years of efforts with considerable investments. The equipment was granted the register and manufacture license by State Drug Administration in 1999. Moreover, this project has been listed as a State High-Tech Industrialization Advanced Project and approved by Science Research Fund of the Ministry of Public Health. The success in clinical application of High Intensity Focused Ultrasound tumor therapy system has realized the dream of non-invasive treatment of tumor. The product has got many patents both in China and abroad. Having been evaluated and demonstrated by senior experts for many times, the clinical application of this technology is considered to have reached world leading level. Through efforts on the research of chemiluminescence analysis, we are the first China-based company to grasp the core technology thereof, and the first to have a platform to develop and manufacture both equipment and reagent. We launched of our Enhanced Chemiluminescence Immunoassay (ECLIA) analysis system and reagents in 2004. We have a modern factory to produce High Intensity Focused Ultrasound tumor therapy system, ECLIA system and reagents and to carry out the R&D of new products. Our company is managed by experienced professional team and talented scientists. We have established nation-wide sale and customer service network. Sustained technical innovation, strict quality control and comprehensive after-sales service constitute our core competence, and create a solid foundation for our healthy growth.

CMED has a market cap of 664 million and a P/E of 26.

{kind=link}

{kind=link}